In summary, the EMIR Refit Regulation 2024 will simplify the reporting requirements under the European Market Infrastructure Regulation (EMIR) for over-the-counter (OTC) derivative transactions. On the 29th of April 2024, it will introduce new reporting obligations and amends derivative transaction reporting requirements.

If you are already captured under the EMIR reporting regime or are in the process of broadening your trading scope to include derivative products, then you will become obliged to comply with EMIR Refit. Here are some steps that banks affected should be taking now to prepare for the upcoming reporting deadlines:

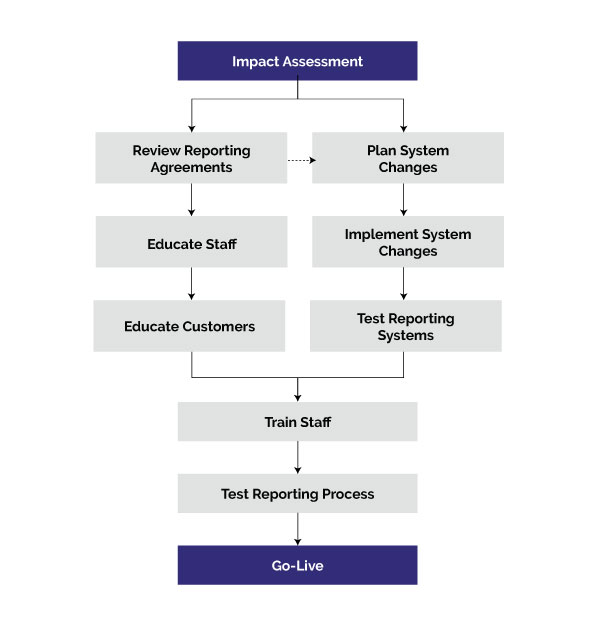

1. Assess the impact

Banks should assess the impact of EMIR Refit on their existing reporting systems, processes, and controls. They need to identify the changes required to comply with the new reporting obligations and ensure IT systems are updated accordingly.

2. Plan systems changes

Enhancements, upgrades and configuration changes to systems are inevitable and could, if not planned early, result in significant risk to projects and if delays are incurred beyond the launch date, significant fines could be levied.

3. Review reporting agreements

Reporting agreements need to be reviewed with relevant stakeholders to ensure that they reflect the new requirements introduced by the EMIR Refit regulation. Changes need to be fully communicated to ensure full compliance.

4. Educate staff

Training needs to be provided to staff on the new reporting requirements and what is needed for compliance. All affected staff need to be sure they understand the importance of accurate and timely reporting of OTC derivative transactions.

5. Educate customers

Banks should seek to educate their customers on any additional data requirements they need to provide under the new EMIR Refit. This includes an understanding of why the regulation is being brought in and will avoid confusion when/if a customer sees new data in their reporting, such as UPIs (Unique Product Identifier), LEIs (Legal Entity Identifier), and the new format for UTIs (Unique Trade Identifier).

6. Test reporting systems

Banks should test their reporting systems to ensure they can capture the new and reformatted data elements required under the EMIR Refit regulation. Testing is also needed to validate the accuracy and completeness of the data to ensure that it meets the regulatory requirements. Full collaboration with trade repositories is key to the testing process.

7. Test the reporting process

The processes behind onboarding new customers also need validating to ensure they work efficiently and are clear and well documented.

8. Monitor compliance

Banks should monitor their compliance with the EMIR Refit regulation on an ongoing basis. They should identify and remediate any issues or errors in their reporting data and ensure that they are reported accurately and in a timely manner.

Some of these activities can be tackled in parallel to compress the timelines. By taking these steps, banks that fall under the reporting regime can ensure they are well-prepared for the new reporting obligations under the EMIR Refit regulation and avoid potential compliance issues.

What you need to know

It is important to not be confused between EMIR and EMIR Refit. There are, in fact, several differences between the two. EMIR Refit is an amendment to the original EMIR regulation and introduces some important changes to the reporting obligations for OTC derivative transactions. Some of the key differences between EMIR and EMIR Refit are:

1. Scope

EMIR Refit extends the scope of the EMIR regulation to include small financial counterparties, such as pension funds, that were previously exempted from reporting obligations.

2. Reporting requirements

EMIR Refit introduces some changes to the reporting requirements for OTC derivative transactions. For example, it introduces new data fields to be reported and changes the timing of reporting for some transactions.

3. Clearing threshold

EMIR Refit raises the clearing threshold for OTC derivatives to EUR 8 billion. This means that counterparties with a lower volume of OTC derivative transactions are not required to clear their transactions through a central counterparty.

4. Risk mitigation techniques

EMIR Refit introduces some changes to the risk mitigation techniques that counterparties must use for OTC derivative transactions. For example, it allows for the use of legally enforceable bilateral netting agreements to reduce counterparty credit risk.

EMIR Refit clarifies the responsibilities of reporting to trade repositories for particular transactions, such as those between a non-EU entity and an EU counterparty.

These are just some of the notable differences between EMIR and EMIR Refit. Banks and other financial institutions must understand these changes and ensure they comply with the updated regulations.

What's the worst that could happen?

The specific fines for non-compliance vary depending on the jurisdiction in which the non-compliance occurs.

- European Union (EU): The European Securities and Markets Authority (ESMA) can impose fines on entities that fail to comply with EMIR Refit reporting requirements. The maximum fine is €5 million or 10% of the total annual turnover of the entity, whichever is higher.

- United Kingdom (UK): In the UK, the Financial Conduct Authority (FCA) can impose fines and sanctions for non-compliance with EMIR Refit. The FCA can impose fines of up to £1 million or 10% of the total annual turnover of the entity, whichever is higher.

- United States (US): The Commodity Futures Trading Commission (CFTC) can impose fines and sanctions for non-compliance with EMIR Refit reporting requirements for entities subject to CFTC jurisdiction. The fines can be up to $1 million per day of violation.

It’s important to note that the fines and sanctions for non-compliance with EMIR Refit can be significant and seriously impact an entity’s reputation and financial standing. Therefore, banks and other financial institutions must ensure that they comply with the EMIR Refit reporting requirements and maintain robust systems and controls to avoid any potential non-compliance.

Final Thoughts

The scale of changes for EMIR Refit is not to be underestimated. Some under-the-hood technical changes with a move to the ISO20022 messaging protocol being introduced will impact existing reporting solutions. Something we will look again at in future blogs. At this stage, early planning and working closely with your solutions providers will ensure you are ready for the new regime on time and with minimum interruption to day-to-day operations.

Book a 30-minute Consultation

Author

Matthew Townsend is the Head of Product for eCommerce, Platform, and Innovation for Banking at Eurobase. With over 20 years of experience in banking technology, Matthew brings a wealth of knowledge and expertise to his role. Matthew has delivered solutions globally across all banking sectors and worked with renowned financial institutions like Deutsche Bank, Rand Merchant Bank, Luminor, Schroders, and neo-banks like N26.

Starting as a developer, Matthew quickly became a functional technical hybrid, bridging the gap between technology and business requirements. Eventually, he transitioned into Product Management as the first Product Manager for Private Wealth at Temenos. Matthew's passion lies in delivering innovative software solutions that meet users' needs and provide a rapid return on investment and value from day one. His experience and dedication make him an accomplished professional in the field of banking technology.